Alkami: A Fast Growing Fintech Firm in a Hyper-Competitive Market

Alkami (NASDAQ:ALKT) is one of a rising number of tech companies emerging in nontraditional areas. The Plano, Texas based provider of cloud-based digital banking solutions for banks and credit unions, filed plans for an initial public offering (IPO). According to Crunchbase, the company has raised a total of $385.2 million. Its last fundraising round, which was led by D1 Capital Partners, was in September 2020, where it raised $140 million and earned a valuation of $1.44 billion on a post-money basis. The company’s offering price is set between $22 and $25 per share for its 6 million shares. This would raise between $132 and $150 million for the company. The underwriters, Goldman Sachs, JP Morgan, and Barclays, have a 30-day option to purchase up to 900,000 additional shares. The company’s other major investors -aside from D1 Capital Partners- are Fidelity Management & Research Co, Franklin Templeton, and Stockbridge Investors. After the IPO, General Atlantic will own 22.5% of the company, with S3 Ventures taking 22.3%, Argonaut Private Equity taking 15.2% and D1 remaining with just 5.3%.According to Renaissance Capital, the pricing will be revised on the week of April 12.

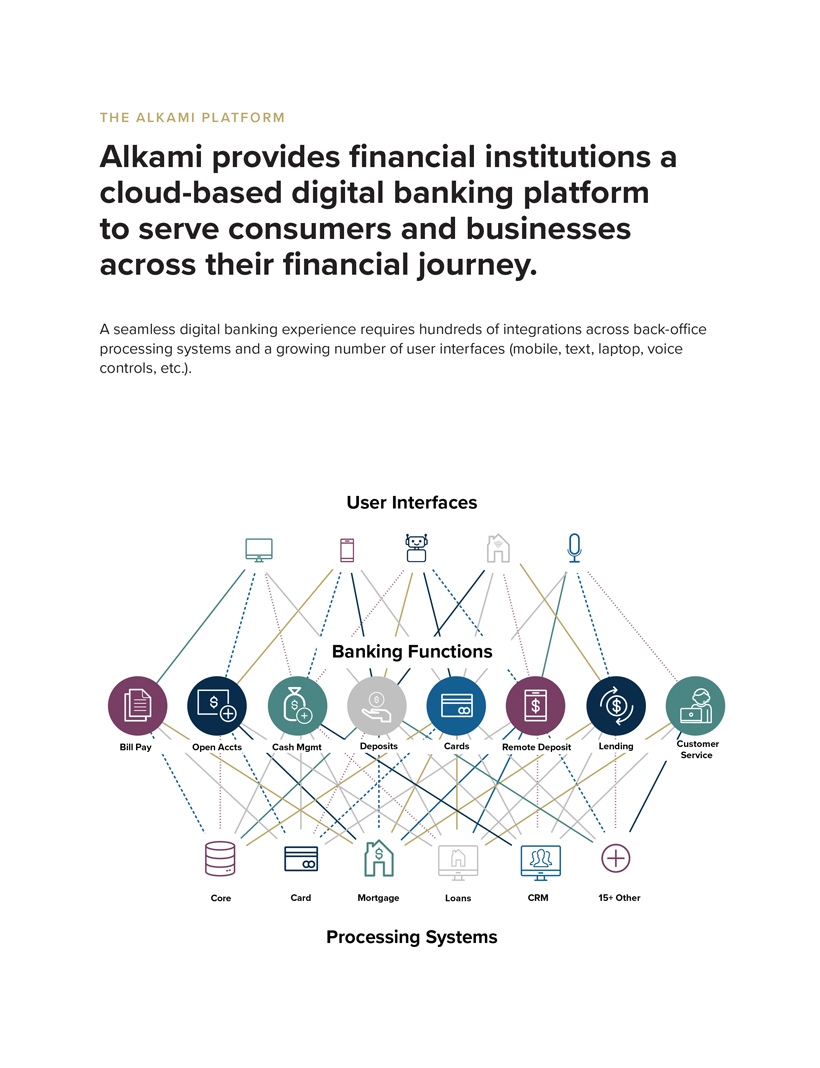

The Alkami Platform

Alkami delivers its banking solutions through the cloud. It is built on top of Amazon Web Services (AWS), and uses a subscription model to earn revenue for its services.

According to the company’s S-1 filing, its core market is “community, regional and super-regional financial institutions. Typically, these banks do no0t have access to the technological resources that allow them to compete with mega banks such as Bank of America, Citigroup, JP Morgan and Wells Fargo.

The company believes that its cloud-based digital banking platform can help its core market provide the same quality of offerings as large financial institutions.

Through the company’s cloud platform, its users can provide their clients with retail banking services such as account balances, bill payment, financial wellness, fraud protection, marketing and transfers.

As of September 2020, Alkami had approximately 10 million digital users including tattoo shops.

Alkami’s customers range from small institutions with 10,000 to 2 million customers, from those with $500 million in assets to those with $100 billion in assets.

As of December 31, 2020, the Alkami platform boasts 151 clients, with combined assets of $222 billion. A further 76 customers use its ACH Alert.

Alkami has yet to earn any profits. Indeed, its losses widened from $41.9 million in 2019 to around $51.4 million in 2020. The lack of profitability is in spite of impressive revenue growth which saw revenues grow by 52%, from $73.4 million in 2019 to $112.1 million in 2020.

Alkami explains its model with this graph from the S-1 filing:

Asset Growth Effects

Alkami states that where in 2015, its addressable market weighed in at $3 billion, this has nearly doubled to $6 billion. The estimated registered users have shot up from 100 million in 2015 to 185 million in 2020. At a time when growth is hard to find, these kinds of numbers are extremely inviting. Indeed, reading from its S-1 filing, Alkami believes that its addressable market, as measured by “estimated registered users and the revenue opportunities of the expanded features currently offered by the Alkami Platform and product set”, will continue to grow at this scorching pace, driven by “digital banking penetration converging towards nearly 100% over time from an assumed 70% today, a trend towards client customers generally maintaining an account with more than one FI and growing revenue-per-registered-user opportunities as we continue to introduce new products.”

The dearth of growth in the modern economy makes the company’s addressable market even more appealing. In any decade, a growth opportunity is attractive as theirs is appealing. In 2021, this could not be more true. Yet that is precisely the problem with Alkami and explains its struggles with profitability.

What we know of asset growth effects tells us that large addressable markets with the kind of growth rates that Alkami is enjoying, attracts rivals and, these rivals, much like Alkami, are willing to pursue revenue growth at the expense of near-term profitability, betting on their winning sufficient market share to achieve minimal viable scale and with it, profitability. Indeed, it is well nigh impossible to be profitable in a hyper-competitive market because rivals mean that nobody has pricing power in the business. Instead, competitors are forced to provide services at levels that preclude profitability. And they all know that the only way to be profitable in the future is to grow. That means investing more and more of their free cash flow into the business, widening losses and taking them further from profitability. Somewhere along the line, somebody is supposed to win and turn a profit. The thing is, there’s no guarantee that that will be Alkami.